Dr Shane Oliver – Head of Investment Strategy and Chief Economist, AMP Capital

Introduction

Successful investing can be really hard in times like the present. Falls in share markets and other assets are stressful as no one likes to see their wealth decline and the natural inclination is to retreat to safety. From their highs last year or early this year to recent lows US and global shares have fallen about 25%. Australian shares have held up better, remaining up from their June low at which point they had had a fall of 16% from their high in August last year, but they remain vulnerable to the lead from global shares. While shares have managed to find technical support in recent days and could bounce further given high levels of negative sentiment, the near-term downside risks for shares remain high, reflecting the same array of macro risks that have been weighing on them all year, notably:

-

high inflation and ultra-hawkish global central banks;

- the $US trending up on safe haven demand and Fed rate hikes risking a financial accident – with mayhem in the UK adding to fears of crisis;

-

an escalation in the Ukraine war, along with other geopolitical risks;

-

high and still rising recession risks; and

-

downwards revisions to earnings ex

-

pectations flowing from all this.

We had a detailed look at the issues a few weeks ago along with signs of light at the end of the tunnel (see here), but I will be the first to admit my crystal ball gets even hazier at times like the present. As always, the turmoil in markets is being met with lots of prognostication. Some of which is enlightening but much is noise. But to borrow one of my favourite quotes that Mark Twain is said to have said “history doesn’t repeat but it rhymes”. While the weakness we are going through differs in detail from rough patches in the past, basic investment principles still apply. It’s hard to say anything new other than to reiterate them. So, apologies if you have seen “seven things for investors to keep in mind” from me before, but at times like this they are worth revisiting.

#1 Share market falls are normal – the key is to make the most of the power of compound interest

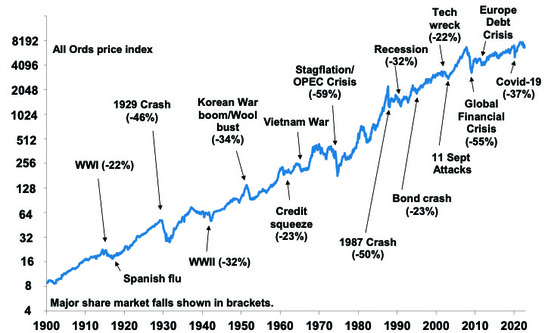

First, while they all have different triggers and unfold differently, periodic share market falls are healthy and normal. Sometimes they are just 5% to 20% corrections, but every so often they can be deep bear markets with falls up to around 50% as in the GFC. But while share market pullbacks can be painful, it’s the way the share market has always been, so they are nothing new. As can be seen in the next chart shares climb a wall of worry over many years but with numerous events dragging them down periodically, but with the long-term rising trend ultimately resuming.

Australian shares have climbed a wall of worry

Source: ASX, AMP

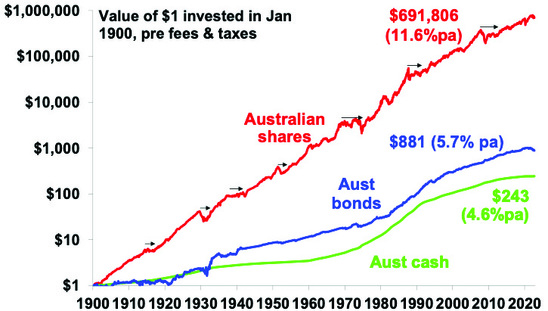

Bouts of volatility are the price we pay for the higher longer-term returns from shares compared to other assets like cash and bonds. The next chart shows the value of $1 invested in various Australian assets in 1900 allowing for the reinvestment of dividends and interest along the way. That $1 would have grown to $243 if invested in cash, to $881 if invested in bonds and to $691,806 if invested in shares. While the average return since 1900 is only double that in shares relative to bonds, the huge difference between the two at the end owes to the impact of compounding returns on top of returns. So, if we want to grow our wealth we need an exposure to growth assets like shares to make the most of the power of compound interest, but with that comes rough patches every so often.

Shares versus bonds & cash over very long term – Australia

Data shown is prior to any fees and taxes. Source: Bloomberg, ASX, RBA, AMP

#2 The key is not to get thrown off by cycles – selling shares after a fall turns a paper loss into a real loss

When shares are falling sharply its naturally tempting to sell. At least it may then be easier to sleep at night. But selling shares or switching to a more conservative investment strategy whenever shares suffer a cyclical setback just turns a paper loss into a real loss with no hope of recovering.

#3 Timing is hard

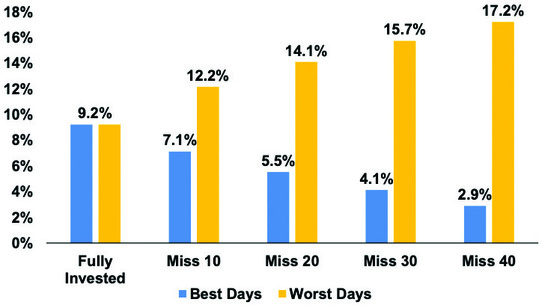

Of course, you may be thinking “but I will reinvest once uncertainty is removed”. But the risk is you don’t feel confident to get back in until long after the market has fully recovered, which may be well above the level you sold out at. Trying to time the market is very difficult. A good way to demonstrate this is with a comparison of returns if an investor is fully invested in shares versus missing out on the best (or worst) days. The next chart shows that if you were fully invested in Australian shares from January 1995, you would have returned 9.2%pa (including dividends but not allowing for franking credits, tax and fees).

Missing the best days and the worst days

Source: Bloomberg, AMP

If by trying to time the market you avoided the 10 worst days (yellow bars), you would have boosted your return to 12.2% pa. If you avoided the 40 worst days, it would have been boosted to 17.2% pa. Fantastic! But this is very hard to do, and many investors only get out after the bad returns have occurred, just in time to miss some of the best days. For example, if by trying to time the market you miss the 10 best days (blue bars), the return falls to 7.1% pa. If you miss the 40 best days, it drops to just 2.9% pa. Hence the old cliché that “it’s time in that matters, not timing”.

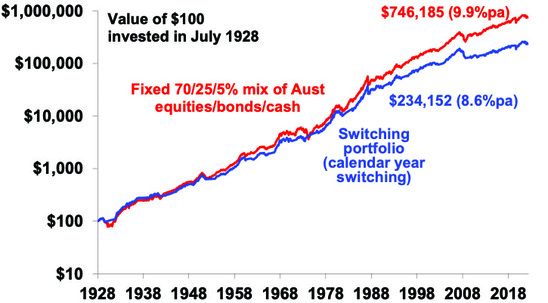

The following chart shows the difficulties of short-term timing in another way. It shows the cumulative return of two portfolios.

-

A fixed balanced mix of 70% Australian equities, 25% bonds, 5% cash;

-

A “switching portfolio” which starts off with the above but moves 100% into cash after any negative calendar year in the balanced portfolio and doesn’t move back until after the balanced portfolio has a calendar year of positive returns. We assumed a two-month lag.

Comparison of constant strategy versus switching to cash after bad times

Source: ASX, Bloomberg, AMP Capital

Over the long run the switching portfolio produces an average return of 8.6% pa versus 9.9%pa for the balanced mix. From a $100 investment in 1928 the switching portfolio would have grown to $234,152 by September but the constant mix would have increased to $746,185.

The best way to guard against selling on the basis of emotion after weakness is to adopt a well thought out, long-term strategy and stick to it.

#4 Share market pullbacks provide opportunities

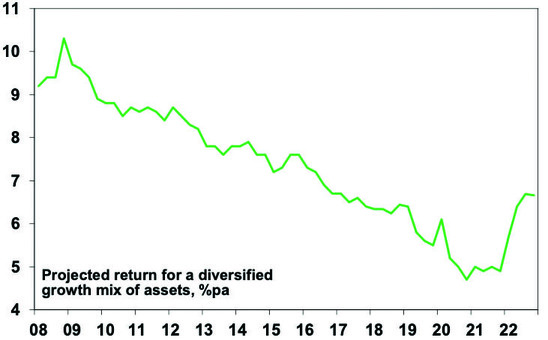

When shares and all assets fall in price, they’re cheaper and offer higher long-term return prospects. As a result of the fall in share and bond prices (and the resultant decline in PEs and rise in dividends yields and bond yields) our estimated medium term return projections for a diversified growth mix of assets has improved from around 4.9%pa to around 6.7%pa. So, the key is to look for opportunities’ pullbacks provide. It’s impossible to time the bottom but one way to do it is to “average in” over time.

Projected medium term returns

Source: AMP

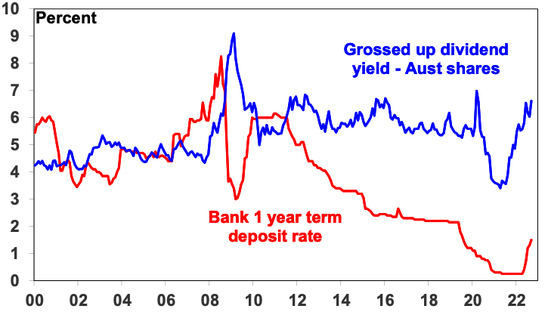

#5 Australian shares offer an attractive dividend yield

This is particularly so compared to bank deposits. Companies don’t like to cut their dividends, so the income flow you are receiving from a well-diversified portfolio of shares is likely to remain attractive, particularly against bank deposits even though deposit rates are slowing rising.

Aust shares still offer an attractive yield versus bank deposits

Source: RBA, Bloomberg, AMP

#6 Shares invariably bottom with maximum bearishness

Shares and other related assets often bottom at the point of maximum bearishness, ie, just when you and everyone else feel most negative towards them. This is when investors have lots of cash on the sidelines which provides fuel for an eventual rebound. This is the point of maximum opportunity. This is obvious in a way because shares could hardly bottom when everyone is already bullish because there would be no one to buy. The problem is that it’s hard for most people to commit to buying shares when there is so much gloom around. And, of course, investor sentiment could still get more negative in the short term before it bottoms.

#7 Turn down the noise

At times like this, negative news reaches fever pitch. Talk of billions wiped off share markets and warnings of disaster help sell copy and generate clicks & views. But we are rarely told of the billions that market rebounds and the rising long-term trend in share prices adds to the share market. Moreover, they provide no perspective and only add to the sense of panic. All of this makes it harder to stick to an appropriate long-term strategy let alone see the opportunities that are thrown up. So best to turn down the noise on all the negative news flow (and watch Elvis films).

Source: AMP Capital October 2022

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.