Why central banks must focus on getting inflation back down

Dr Shane Oliver – Head of Investment Strategy and Chief Economist, AMP Capital

Introduction

I grew up in the 1970s and it was fun – Abba, Elvis, Wings, JPY, flares, cool cars, etc. But economically it was a mess. Inflation surged and so did unemployment. And it was bad for investors too. After years of economic pain voters turned to economically rationalist political leaders – like Thatcher, Reagan and Hawke & Keating – to fix it up. Their policies to boost productivity ultimately culminating in independent inflation targeting central banks along with the help of globalisation, more competitive workforces and the IT revolution got inflation under control from the 1980s and 1990s. So much so that there was even talk of “the death of inflation”. The experience of the last year when inflation has surged tells us that unlike the parrot in Monty Python it really wasn’t dead but just resting. Initially its rise was seen as “transitory”. And many are still questioning why central banks need to do much – what will RBA rate hikes do to bring high lettuce prices back down? – and that central bank worries about wages growth picking up causing a wage price spiral are just a baby boomer fantasy. So just sit it out. The 1970s experience suggests otherwise.

So what happened in the 1970s?

Many associated the inflation of the 1970s with the oil shocks of 1973 and 1979 but it actually got underway before that.

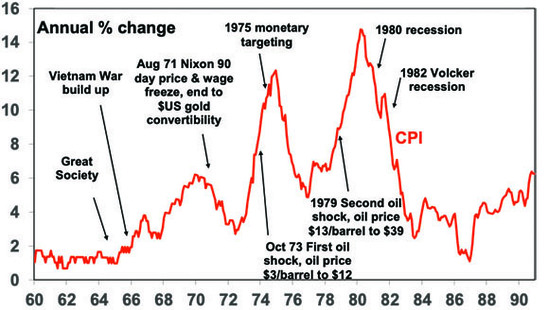

US inflation, 1960 to 1990

Source: Bloomberg, AMP

From around the mid-1960s inflation started moving up, notably in the US and then later in Australia reflecting a combination of:

-

A big expansion in the size of government and welfare.

-

Disruption associated with the Vietnam War.

-

Tight labour markets (with unemployment falling to 3.4% in 1969 in the US and spending most of the 1960s below 2% in Australia) led to more militant workers and surging wages.

-

Easy monetary policies which supported high inflation.

-

Social unrest & industry protection also played a role.

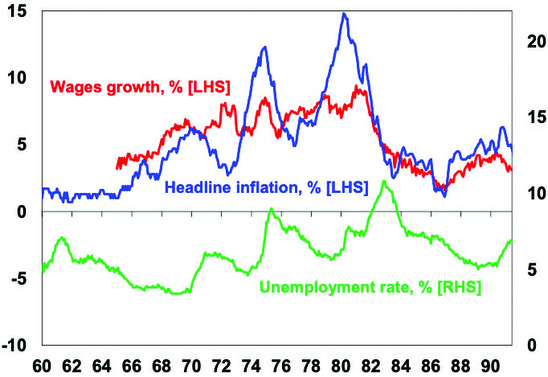

From 1965 to 1969 US inflation rose from below 2% to above 6%. US monetary policy was tightened driving a recession in 1969-70 which saw inflation dip. Monetary policy was then eased but before inflation came under control so it bottomed well above 1960’s lows and started up again forcing a return to monetary tightening. In 1973 inflation had already increased to 8% before the OPEC shock. The same whipsaw happened after another recession in 1974-75 which saw inflation bottom out above its previous high only to take off again. The process only ended with the deep recessions of the early 1980s.

US inflation, wages grth & unemployment, 1960-90

Source: ABS, AMP

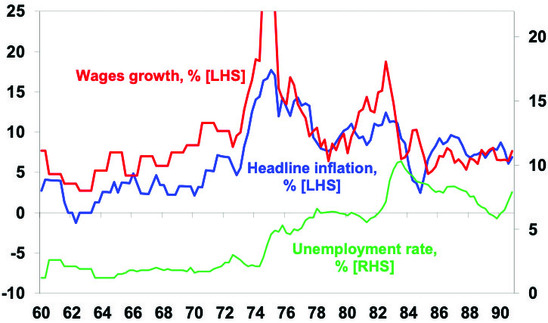

It was pretty much the same story in Australia, although here it started more in the early 1970s and was made worse by 20% plus wages growth and massive fiscal stimulus in 1974.

Australian inflation, wages grth & unemployment, 1960-90

Source: ABS, AMP

And in Australia, the automatic indexation of wages to inflation from 1975 just helped lock in high inflation (as wages add to costs) with only the 1983 Accord breaking the nexus by trading off wage increases for tax cuts and social benefits.

The end result was a decade of high inflation and high unemployment. The problem was that policy makers were too slow to realise the extent of the inflation problem initially and then were too quick to ease which enabled inflation to quickly pick up again and move higher. The longer inflation persisted the more inflation expectations rose – with wage growth rising – making it harder to get inflation back down.

Why the concern today?

There are several reasons for concern about a return to the sustained high inflation of the 1970s today:

-

Labour markets are very tight once again. Wages growth in the US has already increased to around 5%.

-

Demand has been strong suggesting that the problem is not just due to supply disruptions.

-

We are seeing a run of supply shocks – with notably the war in Ukraine, another energy crisis & repeated floods locally.

-

Government policy has swung away from the economic rationalist approaches of the 1980s – with more tolerance for bigger more interventionist government – as median voters have swung back to the left.

- The globalisation that followed the end of the USSR and trade with China is under threat and appears to be reversing, not helped by a desire to onshore supply chains.

-

This is being reinforced by geopolitical tensions which are boosting defence spending which adds to metal demand.

-

Decarbonisation will boost near term costs & metal demand.

-

The ratio of workers to consumers is falling and the entrance of millennials to the workforce replacing retiring baby boomers will depress productivity (just as the boomers did in the 1970s).

-

Policy makers were caught focussing on the last war of disinflation coming out of the pandemic just as they were in the 1960s when the big fear was a return to 1930s deflation. This saw massive fiscal stimulus and money supply growth.

-

Inflation is now very high at around 9% in the US, Europe and UK and an estimated 6% in Australia and as we saw in the 1970s the longer it remains high the more businesses and workers will expect it to remain high and they will plan accordingly. That is, inflation expectations will move up, which will make it harder to get inflation back down.

So while central banks can’t do much to boost the supply of lettuces and lower petrol prices they are right to have moved to a more aggressive strategy as it will slow demand and by stressing that they are committed to returning inflation to target will help keep inflation expectations down.

Why high inflation is bad news for investors?

The 1970s experience warns it’s in investors long term interest to get inflation under control even if it involves a bit of short term pain. For investment markets high inflation is bad as it means:

-

Higher interest rates – which makes cash more attractive and other assets relatively less attractive.

-

Higher economic volatility and uncertainty – the period from 1969 to 1982 saw four recessions in the US and three recessions in Australia. This means that investors will demand a higher risk premium to invest.

-

For shares, a reduced quality of earnings as firms tend to understate depreciation when inflation is high.

The first two mean rising bond yields which means capital losses for investors in bonds. This tends to unfold gradually.

All three mean shares tend to trade on lower price to earnings multiples when inflation is high, and real growth assets (like property) generally tend to trade on higher income yields. This was seen in the high inflation 1970s when shares struggled. It means that the boost to earnings (or say rents in the case of property or infrastructure) from inflation tends to be offset by a negative valuation effect as investors demand lower PEs/higher yields. See here for a deeper explanation.

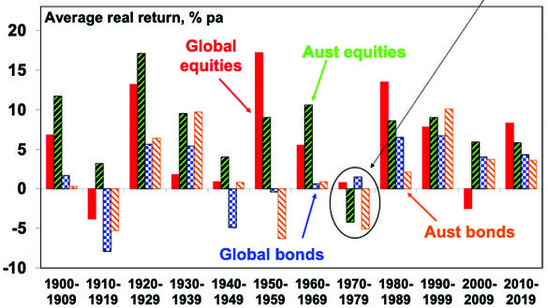

So the bottom line is that a sustained period of high and rising inflation can be a problem for bonds, shares and other growth assets. As can be seen in the next chart, the high inflation 1970s was one of the few decades to see poor real (ie after inflation) returns from bonds and shares.

The 1970s saw poor returns from shares and bonds

Source: Global Investment Return Yearbook ABN/AMRO, Bloomberg, AMP

So, it’s in investors’ interest that inflation is kept low and stable.

Reason for optimism a return to the 1970s is unlikely

While many of the structural forces that drove the disinflation of the last few decades are reversing and suggest higher inflation over the decade ahead than seen pre-pandemic, sustained 1970s style high inflation appears unlikely:

-

Central banks understand the problem and the need to keep inflation expectations down, and are now committed to bringing inflation back to target with Fed saying the commitment is “unconditional” (even if it means a recession) and the RBA saying it will do “what is necessary”.

-

While inflation is high, longer term inflation expectations remain low (at 3.1% in the US compared to nearly 10% in 1980) and wages growth is still relatively low suggesting it should be easier to bring inflation down than it was in 1980.

US University of Michigan Consumer Inflation Expectations

Source: Macrobond, AMP

-

Related to this labour markets are far more competitive today with much lower levels of unionisation. In Australia, only 14.3% of employees (including me) are in a union whereas in 1976 it was at 51% of employees.

-

Finally, as we noted here there are signs of easing cyclical inflation pressure in the US & its leading by about 6 months.

So, while inflation may not go back to pre-pandemic lows and the longer-term tailwind for investment markets from ever lower inflation and interest rates may be behind us, a full on return to the 1970’s malaise looks unlikely.

Source: AMP Capital July 2022

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.