The US election is only a month away. Markets are now paying close attention to it for several reasons. First, Joe Biden is proposing higher taxes and more regulation. Second, the proximity of the election made worse by the move to replace Justice Ginsberg may have reduced prospects for needed fiscal stimulus. Third, increased use of postal voting could mean it will take longer before the outcome is known. Finally, President Trump’s scorn for postal voting (which polls show 45% of Biden voters plan to use versus 10% of Trump voters!) looks to be setting up a challenge to the result if he loses and his refusal to guarantee a peaceful transfer, adds to uncertainty.

Polls and betting odds favour Biden

-

Real Clear Politics poll average has Biden ahead by 6 points. This is down from around 9 points since July as Trump got a boost as the daily number of new coronavirus cases fell from nearly 70,000 to 40,000 but it’s been pretty stable over the last two months. This contrasts with four years ago where polls mostly had Clinton ahead, but it was very volatile with Trump out front on several occasions. In late September 2016 Clinton was about 2.5 points ahead.

Source: Real Clear Politics

-

Biden’s lead averages about 3 points in battleground states.

-

The ‘Predict It’ betting market has Biden with a 17 point lead but has a Democrat clean sweep (where it wins the presidency, House and Senate) at around 50/50. The Democrats already have control of the House and are likely to retain that, but they need three seats with the Vice President, to gain a majority in the Senate. A clean sweep would remove the Senate as a blockage to higher taxes.

-

Nate Silver’s 538 election model that combines state polls with economic data puts a Biden win at 78% probability.

-

More shy Trump voters than Democrat voters in revealing their true intention adds to the uncertainty around polls.

-

The first debate didn’t offer anything new on the policy front and is unlikely to have changed things much.

The economy versus the virus

History indicates incumbent presidents tend to lose when there is a recession in the two years before the election.

Source: Strategas

However, Trump’s best hope is for a rebound in the economy, with data pointing to an 8% rebound in September quarter GDP (due just before the election) thereby ending the recession. There has been a precedent for incumbent presidents being re-elected if the recession ends prior to election day. But it’s only 50/50 and was early last century – with Presidents McKinley in 1900, Roosevelt in 1904 and Coolidge in 1924 getting re-elected as recessions ended prior to the election but not so for Presidents Taft in 1912, Ford in 1976 and Carter in 1980. Working against this for Trump would be if the recent resurgence in US new coronavirus gathers pace resulting in renewed uncertainty about the economic outlook.

Source: RCP, ourworldindata.org, AMP Capital

The US share market is sending a more positive signal for Trump. It has been one of the best guides to the election outcome – if the S&P 500 is up over the 3 months prior to the election date the incumbent party tends to win and vice versa if it’s down. This has been 87% accurate since 1928 and 100% accurate since 1984. Right now, its up 1.2% since August 3rd!

Bottom line: Biden is ahead but its premature to write Trump off.

Key Biden policy directions versus Trump

Taxation: Biden plans to raise the corporate tax rate to 28% (from 21%), return the top marginal tax rate to 39.6% (from 37%) and tax capital gains and dividends as ordinary income.

Infrastructure: Both plan to spend $1trn or more over 10 years on infrastructure with Biden focussed on renewable energy.

Climate policy: Biden aims for the US to reach net zero emissions by 2050 by raising the cost of fossil fuels & boosting the development of alternatives (possibly with a carbon tax)

Regulation: Biden is likely to end the era of deregulation.

Coronavirus: Biden is likely to oversee a more robust, organised and consistent response to dealing with the virus.

Healthcare: Biden wants to strengthen Obamacare.

Trade and foreign policy: A re-elected Trump is likely to ramp up his trade war with China with “made in America” tax credits and more tariffs on imports on China and possibly elsewhere including Europe. By contrast, Biden would likely rebuild the alliance with Europe, work with international organisations like the World Trade Organisation, work to re-establish the nuclear deal with Iran and adopt a more diplomatic approach to dealing with issues with China (working with Europe and Asian allies).

Budget deficit: For the near term, the budget deficit is likely to remain high whoever wins, but historically they have fallen under Democrats after rising under Republicans. That said, if the economy proves slow to recover, Joe Biden may be more likely to respond with large public sector spending programs.

Economic impact of a Biden victory

Higher tax rates and more regulation under Biden would be negative for the growth outlook on their own. However, as with all things economic, it’s never as simple as that.

-

First, the negative impact of tax hikes and increased regulation in the short term could be more than offset by increased infrastructure spending.

-

Second, once in office Biden will likely delay or dampen down his planned tax hikes, given the weak economy.

-

Third, raising taxes on top earners, while a negative for incentive, may help reduce inequality.

-

Fourth, Biden’s trade and foreign policy focused on strengthening ties with allies and a diplomatic approach to China will reduce a source of angst and uncertainty under Trump (which will likely intensify if he is re-elected).

-

Finally, more stable and predictable policy making under Biden may provide a more certain environment for business and so result in increased business investment.

So, I see no reason to expect a weaker economic/investment outlook under Biden beyond near-term uncertainty.

Likely market reaction

Since 1927, the election year has been reasonable for shares with an average total return of 11.2% pa. Of course, this year is complicated by coronavirus & this election comes with greater than normal uncertainty. There are several points to note.

First, the next month or so could see continued volatility and the correction in shares may have further to run:

-

if it’s going Biden’s way investors are likely to fret more about the prospects of higher taxes & regulation, particularly if it looks like Democrats will win control of the Senate;

-

if it’s close and contested it may be a while before the winner is known and markets won’t like the uncertainty; and

-

Trump may also refuse to go peacefully as he’s signalled.

Second, while delays in counting postal votes may mean it takes longer to get a result (which under one scenario could see counting first go in Trump’s favour and then in Biden’s as more postal votes are counted), Trump’s refusal to guarantee to go peacefully should be taken “seriously but not literally” – it’s hard to see him starting a civil war and senior Republicans have not supported him on this with Senate majority leader McConnell saying “there will be an orderly transition just as there has been every four years since 1792.”

Third, if ultimately Trump is the winner, US shares may initially celebrate and outperform global and Australian shares but would be vulnerable next year as the trade war with China ramps up again. By contrast, after an initial negative reaction if Biden wins, for the reasons already noted, there is no reason to expect a weaker economy, and hence share market, under a Biden presidency.

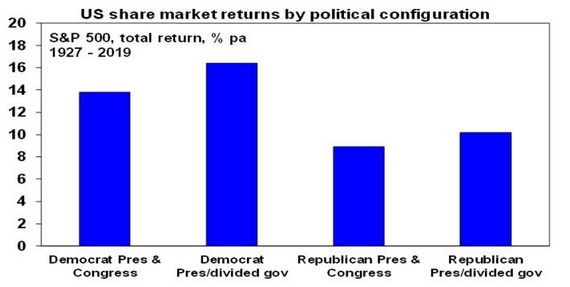

Finally, historically US shares have done best under Democrat presidents with an average return of 14.6% pa since 1927 compared to an average return under Republican presidents of 9.8% pa. The best average result (16.4% pa) has actually occurred when there has been a Democrat president and Republican control of the House, the Senate or both.

Source: Bloomberg, AMP Capital

Concluding comment

The US election has the potential to create further volatility in investment markets. A Trump victory will mean more of the same and at least initially would probably be more positive for US shares than global and Australian shares (all other things being equal). By contrast a Biden victory may add to short-term volatility but this is likely to be short lived as there is no reason to expect a weaker economy and hence share market under a Biden presidency and he is likely to take a less disruptive approach to trade and foreign policy issues.

Source: AMP Capital 30 September 2020

Important notes: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) (AMP Capital) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent of AMP Capital.