This economic and fiscal update is the first since December’s Mid-Year Economic and Fiscal Outlook when budget surpluses looked just around the corner. Since then things have changed dramatically due to the hit from coronavirus and necessary support measures from the Government.

Policy stimulus

The statement provided no new policy stimulus measures beyond those that have been announced in the last two weeks:

-

$2bn in spending on subsidies for apprentices & JobTrainer;

-

An estimated $16bn to extend JobKeeper to March next year but with payments stepping down to $1200 and then $1000 a fortnight for those who worked 20 hours or more per week in February and to $750 and then $650 for others and businesses having to meet the turnover reduction test at the end of the September and December quarters to keep receiving it; and

-

An estimated $3.8bn to extend the JobSeeker Supplement to December at the pared back rate of $250 a fortnight.

This additional $22bn in spending along with prior coronavirus-related economic support (in the form of actual spending, tax breaks and health measures) takes the COVID-19 response package to nearly $174bn. JobKeeper is the main element in this, but it also includes the JobSeeker supplement, payments to businesses and payments to eligible households. There is also loans & guarantee support (from the government and RBA) worth $125bn or just over 6% of GDP.

Proposals to bring forward the tax cuts and provide additional investment incentives look to have been pushed out to the October budget and additional industry support packages are also likely. The Government may have delayed this extra stimulus to gauge how much additional help will be required with a lot riding on how quickly the latest outbreak of coronavirus is brought back under control. Spreading out the announcement of new stimulus measures may also get more bang for the buck in terms of the boost to confidence.

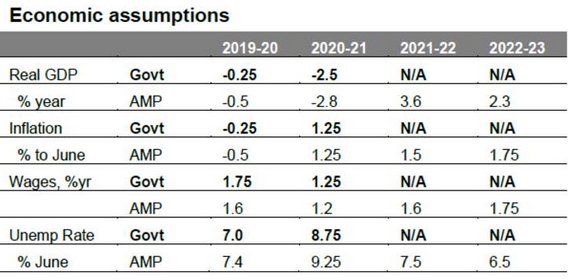

Economic assumptions

The Government is forecasting the economy to contract this financial year by -2.5%, its biggest financial year contraction since 1946-47. But this masks a “record” -7% contraction in June quarter GDP and a gradual recovery from the second half of this year. The Government is a bit more optimistic than we are in terms of economic growth and unemployment.

Source: Australian Treasury, AMP Capital

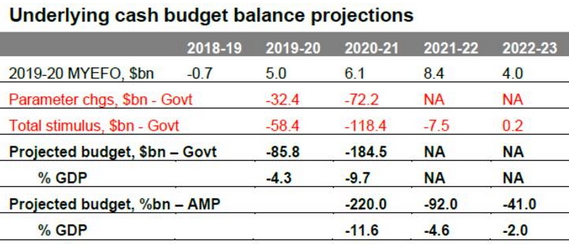

Budget deficit projections

The Government’s revised budget projections and our own are shown below. These should be treated with greater than normal caution given the uncertain economic outlook.

Source: Australian Treasury, AMP Capital

The hit to the economy and hence revenue and expenditure since the Mid-Year Economic and Fiscal Outlook last December is huge at $72bn for this financial year and is shown in the line called “parameter changes”. It should gradually start to diminish as the economy recovers. Policy stimulus (mainly due to the coronavirus response but also other things) since last December is shown in the line labelled “Total stimulus”.

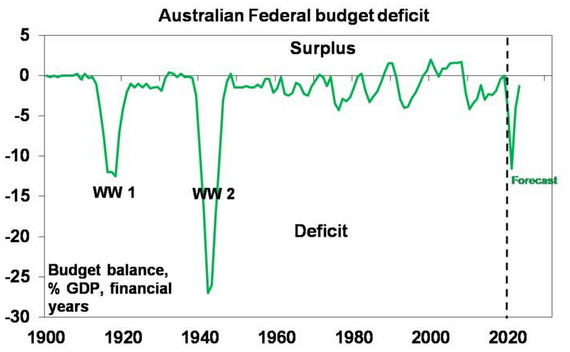

As a result of the Government’s fiscal response and the hit to revenue from the economic downturn, the Government projects the budget deficit to further blow out from around $86bn for the past financial year to a record $184.5bn this financial year.

While it does not provide projections beyond this financial year the implication is that the deficit will decline in future years as support programs phase down and the economy recovers. On the Government’s projections this would see the budget deficit as a share of GDP peak at around 9.7% of GDP in 2020-21, which would be its highest since World War 2. We continue to see a bigger deficit for this financial year of around $220bn reflecting both a bigger hit to revenue and additional stimulus of around $17bn to be announced in the months ahead, including in the October budget. This is likely to include the bring forward of the 2022 tax cuts, more investment incentives and more industry support programs. The budget deficit blow-out will add about 20% of GDP to public debt out to 2022.

Source: RBA, Australian Treasury, AMP Capital

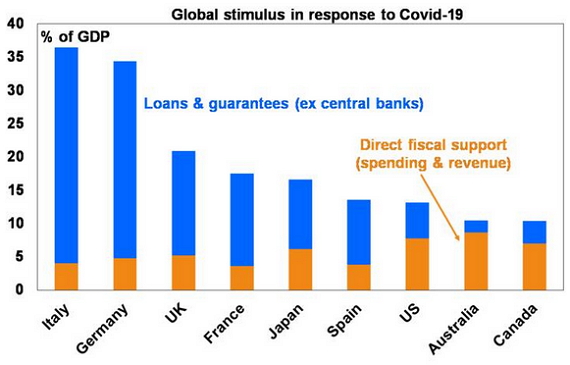

Assessment

The additional $22bn in stimulus announced over the last two weeks is welcome and will help turn the fiscal cliff in October into a fiscal slope. The boost to stimulus announced in the last two weeks takes Australia’s total level of coronavirus related fiscal stimulus (excluding loans and guarantees) this year up to 8.7% of GDP, which is well and truly at the high end of comparable countries. This should aid the economic recovery.

Source: IMF, AMP Capital

However, it’s doubtful that this will be enough given the long tail of unemployment flowing from the coronavirus shock. We estimate that were it not for JobKeeper and people leaving the workforce the effective unemployment rate would currently be 11.3%, which is well above the official measured rate of 7.4%. This has fallen from 14.8% in April thanks to the reopening of the economy, but with the threat to the recovery posed by the second wave of cases in Victoria and the lockdown in Melbourne and the risk of a flow on to NSW, effective unemployment may only fall to around 10% or so by September and maybe 9% or more going into next year, so continued income support is essential. The Government’s focus now shifts to economic reforms in the October budget and this is likely to include even more fiscal support, as noted earlier.

Source: IMF, AMP Capital

Our assessment remains that the blow out in the budget deficit is affordable. First, it’s absolutely necessary as were it not for the support measures the economic hit would be far greater.

Second, it makes sense for the public sector to borrow from households and businesses at a time when they have cut their spending, and to give the borrowed funds to help those businesses and individuals that need help.

Third, the support programs are targeted at current needs so shouldn’t lead to permanently higher government spending.

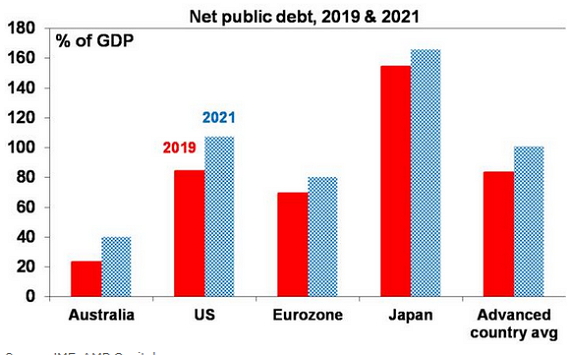

Fourth, Australia’s starting point for net public debt last year was low at 23% of GDP compared with other advanced countries averaging 83%. See the next chart. And even with projected budget deficits it will remain relatively small.

Source: IMF, AMP Capital

Fifth, borrowing to finance the budget deficit is in Australian dollars and we are not dependent on foreign creditors, so we are not vulnerable to a “foreign currency crisis.”

Finally, the cost of Government borrowing is very low at around 0.85% for ten years and 0.25% for three years.

Implications for the RBA

Ongoing Government support for households and businesses is not enough to change our assessment that the RBA will need to keep cash rate near zero for years ahead and possibly need to undertake more quantitative easing in the face of ongoing spare capacity in the economy and below target inflation.

Implications for Australian assets

Cash and term deposits – with the cash rate unlikely to rise from 0.25% for years, returns from cash and bank term deposits will remain low for a long time to come. That said the budget stimulus and increase in money supply holds out at the prospect that at some point inflation and interest rates will rise. But it’s probably at least three years away.

Bonds – the surge in public debt and bond supply would all other things being equal, point to higher bond yields, but this is offset by massive spare capacity, low private sector borrowing, very low inflation and the cash rate capped at 0.25% for years it’s hard to see a lot of upside in bonds yields. That said, if coronavirus comes under control it’s hard to see a lot of downside either so medium-term bond returns are likely to be low.

Shares – the addition of extra policy stimulus further helps to offset the hit from coronavirus and adds to confidence that growth will recover which is supportive of shares.

Property – ongoing income support is continuing to help the property market avoid a sharp fall in home prices but the negatives around high effective unemployment, the weak rental market and the collapse in immigration point to ongoing falls in prices into next year, particularly in Sydney and Melbourne.

The $A – ongoing fiscal stimulus at the high end of comparable countries coming at a time of rising commodity prices and a declining US dollar point to more upside for the $A.

Concluding comment

With private sector spending hit by coronavirus it makes sense for the Government to continue to help fill the breach and support the economy. The best approach to getting debt back down is to grow the economy aided by a reinvigorated economic reform agenda, but for a while yet government fiscal support will continue to be needed.

Source: AMP Capital 23 July 2020

Important notes: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) (AMP Capital) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent of AMP Capital.