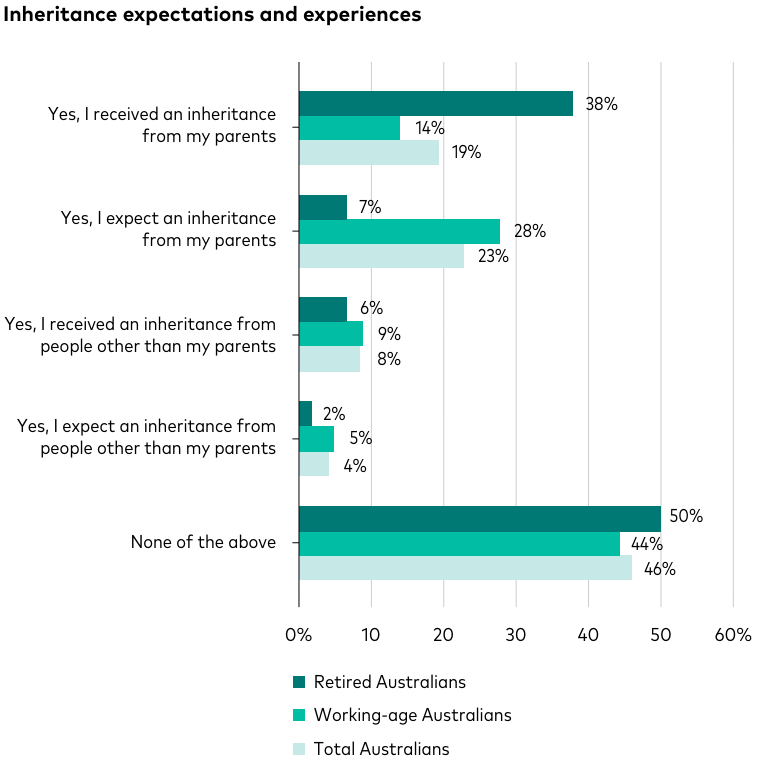

Many Australians expect an inheritance, but their parents may have a different view.

Around one in two Australians have received or expect to inherit money or property, either from their parents or others.

That’s one of the key findings from Vanguard’s 2024 How Australia Retires research, but it shouldn’t come as a great surprise.

Over the coming years trillions of dollars of assets are likely to be shifted from the estates of deceased older Australians to their children and other heirs. Most of this will be in the form of residential real estate, unspent superannuation savings, and other investment assets.

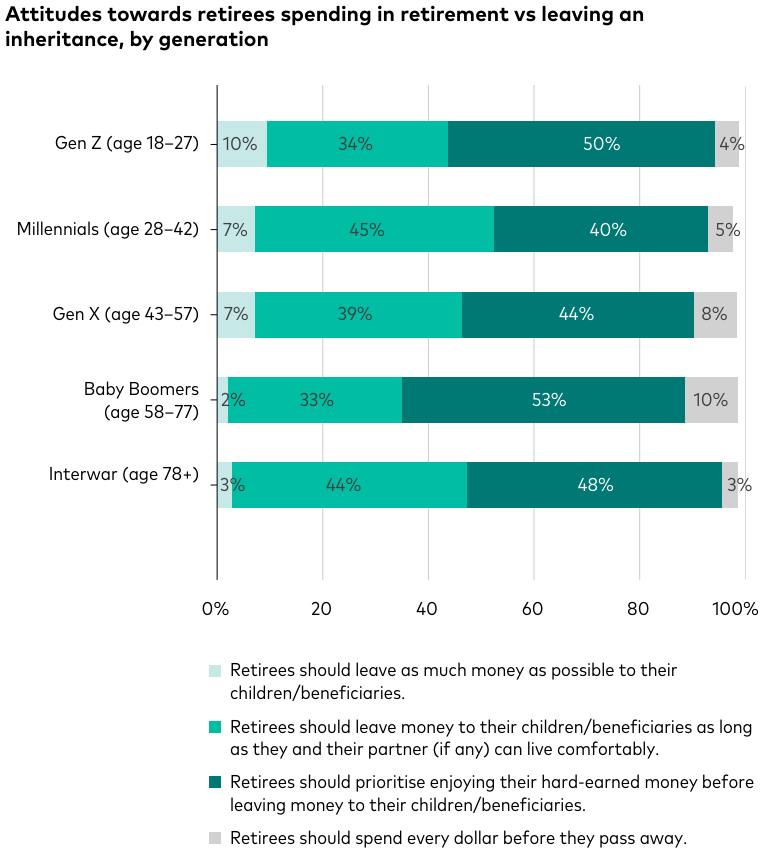

But, when it comes to leaving inheritances, it’s clear there are differing views across generations on whether parents should spend as much as they can before they die or conserve their spending so more assets can be passed on to their children.

Vanguard surveyed more than 1,800 working and retired Australians aged 18 years and over in March this year and asked them about their attitudes towards retirees spending their money versus leaving an inheritance.

Almost half of the people surveyed said they believe retirees should prioritise their own spending before leaving money to their children or beneficiaries.

But behind that number is a general expectation by 38% of the survey respondents that retirees should leave money aside for inheritances, as long as they can live comfortably.

Only 6% of those surveyed said that leaving an inheritance should be the primary goal for retirees, and that they should leave behind as much money as possible to their heirs.

About the same percentage (7%) believe retirees should spend all of their money (SKI) before they pass away.

What generations are thinking

What’s quite interesting are the differing attitudes across generations on whether retirees should spend the kids’ inheritance (go “SKI”ing) or keep money aside for their beneficiaries.

10% of Baby Boomers (aged 58 to 77) in Australia believe retirees should spend all of their money in retirement, while 10% of Gen Z (aged 18 to 27) believe retirees should leave as much money as possible to their children/beneficiaries.

At the other end of the spectrum, more Millennial (aged 28 to 42) and Gen X (aged 43 to 57) Australians than older generations believe retirees should leave as much money as possible to their children and beneficiaries.

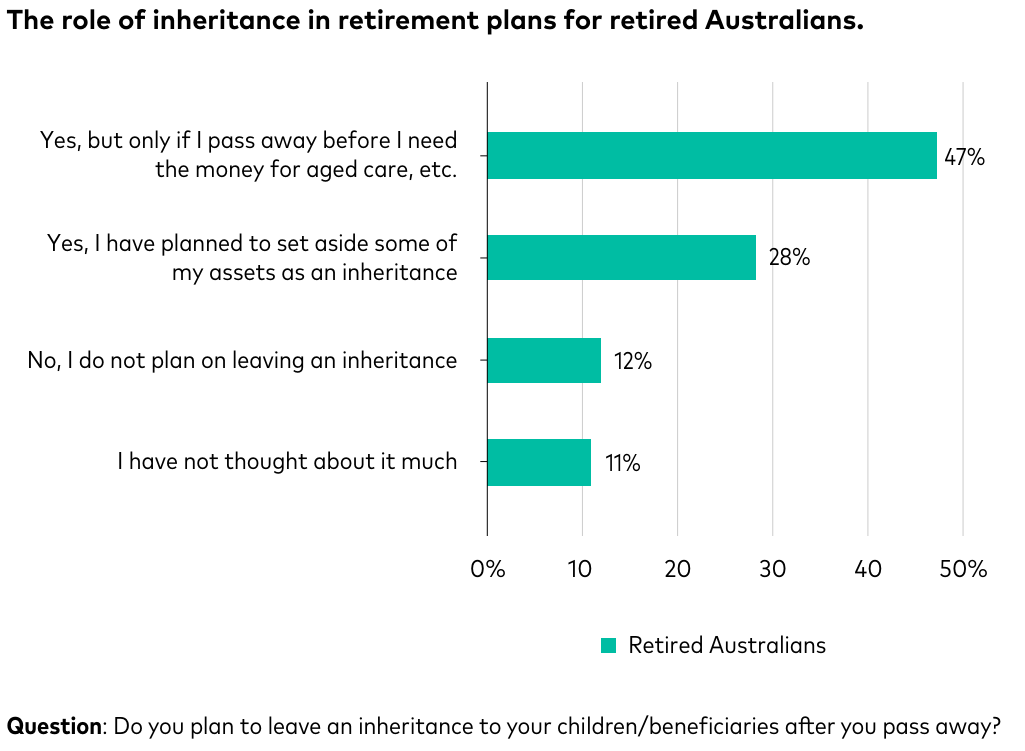

Most retirees want to leave an inheritance

When it comes to incorporating inheritances into retirement planning, 47% of retirees plan to do so.

But most retirees surveyed said they could only do so if they passed away before they needed their money for aged care and other expenses.

28% of retirees, on the other hand, have planned to set aside some of their assets as an inheritance, while 12% said they do not plan to leave an inheritance at all.

Superannuation death benefits on the rise

The conversation around inheritances interweaves with Australian government research that many Australians are not exhausting their superannuation savings before they die.

The 2023 Intergenerational Report found that most retirees draw down at the legislated minimum drawdown rates.

“This results in many retirees leaving a significant proportion of their balance unspent, for example, a single retiree drawing down at the minimum rates would be expected to still have a quarter of their retirement assets at death,” the report noted.

Additionally, the 2020 Retirement Income Review included projections from Treasury that outstanding superannuation death benefits could increase from around $17 billion in 2019 to just under $130 billion in 2059, assuming there’s no change in how retirees draw down their superannuation balances.

This is where good estate planning, using the services of professionals such as a lawyer, financial adviser, and a tax practitioner, really comes to the fore.

For example, leaving superannuation to non-dependents can have tax consequences for beneficiaries.

There’s a lot to be said for having open discussions within your family about the intended treatment of assets and future inheritances.

Beyond accumulating wealth over time, one of the most important aspects of estate planning is determining in a legally valid will how you intend to have your accumulated wealth distributed after your death.

Speak to us today for more information.

Source: Vanguard June 2024

This article has been reprinted with the permission of Vanguard Investments Australia Ltd. Copyright Smart Investing™

GENERAL ADVICE WARNING

Vanguard Investments Australia Ltd (ABN 72 072 881 086 / AFS Licence 227263) (VIA) is the product issuer and operator of Vanguard Personal Investor. Vanguard Super Pty Ltd (ABN 73 643 614 386 / AFS Licence 526270) (the Trustee) is the trustee and product issuer of Vanguard Super (ABN 27 923 449 966).

The Trustee has contracted with VIA to provide some services for Vanguard Super. Any general advice is provided by VIA. The Trustee and VIA are both wholly owned subsidiaries of The Vanguard Group, Inc (collectively, “Vanguard”).

We have not taken your or your clients’ objectives, financial situation or needs into account when preparing our website content so it may not be applicable to the particular situation you are considering. You should consider your objectives, financial situation or needs, and the disclosure documents for the product before making any investment decision. Before you make any financial decision regarding the product, you should seek professional advice from a suitably qualified adviser. A copy of the Target Market Determinations (TMD) for Vanguard’s financial products can be obtained on our website free of charge, which includes a description of who the financial product is appropriate for. You should refer to the TMD of the product before making any investment decisions. You can access our Investor Directed Portfolio Service (IDPS) Guide, Product Disclosure Statements (PDS), Prospectus and TMD at vanguard.com.au and Vanguard Super SaveSmart and TMD at vanguard.com.au/super or by calling 1300 655 101. Past performance information is given for illustrative purposes only and should not be relied upon as, and is not, an indication of future performance. This website was prepared in good faith and we accept no liability for any errors or omissions.

Important Legal Notice – Offer not to persons outside Australia

The PDS, IDPS Guide or Prospectus does not constitute an offer or invitation in any jurisdiction other than in Australia. Applications from outside Australia will not be accepted. For the avoidance of doubt, these products are not intended to be sold to US Persons as defined under Regulation S of the US federal securities laws.

© 2024 Vanguard Investments Australia Ltd. All rights reserved.