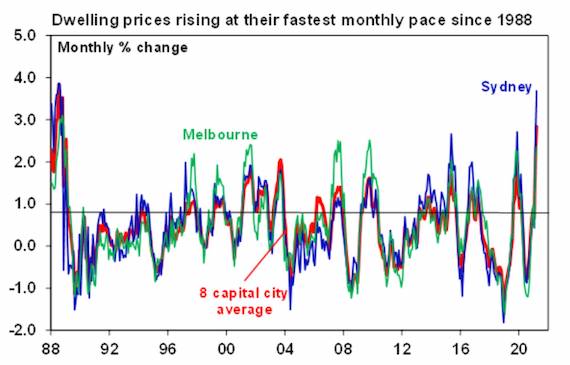

Average dwelling prices in Australian capital cities rose by 2.8% in March, their seventh consecutive monthly gain and the largest in more than 30 years. Prices are now up by 3.5% on previous record highs and almost 5% on pre-pandemic levels. Homeowners across the country are sharing in the good fortune, with Perth and Darwin the only two cities where residential property prices have not recently surpassed their previous high-water marks. Incredibly, regional markets have run even stronger over the past twelve months, up 11.4% on a year ago.

Source: CoreLogic, AMP Capital

Other indicators, including new housing finance commitments, sales volumes and clearance rates, support the narrative laid out by prices: the Australian housing market is booming again, following a brief fall of about 3% in the midst of the deepest recession since the 1930s.

The dominant player in this narrative has been, for the most part, the record low-interest rate environment. Loan serviceability has benefited immensely, with household interest payments as a percentage of disposable income at its lowest level since the 1990s, and low discount rates have improved the attractiveness of rental yields.

But for the moment low interest rates are mostly a given, since the RBA has indicated that it will keep them on hold until the economy records inflation figures within the target band of 2-3%. So, to determine reasons behind this boom and its likely trajectory over the next couple of years, it makes sense to take a closer look at a number of the other non-monetary factors at play.

Government support packages

Most Australians probably appreciate the extent to which JobKeeper has kept the country afloat over the past year, and if its removal continues to proceed without too much drama it will have been something of a victim of its own success (or is that design!). Other, less prominent, programs have also been put in place to support the housing industry over the period, including HomeBuilder (which was phased out with JobKeeper at the end of March), the First Home Loan Deposit Scheme (which is now tapped out) and a number of state-funded equivalents.

The winding back of these programs may still dampen the market a little, but their work is largely done, and in the absence of a significant new lockdown the impact should be marginal. Actual net job losses from the ending of JobKeeper are likely to be low and the proportion of loans at risk is minimal, as demonstrated by the fact that the value of home mortgages still relying on payment holidays had declined from 11% in May 2020 to less than 1%1 by the end of February.

Australia’s budding economic recovery

Recent labour force numbers show employment nearly back to pre-pandemic levels, and the rate of unemployment settling into what we expect will be its steady state as long as minimal disruption from the pandemic continues. And according to 2020’s December quarter GDP numbers, our economy had recovered to such an extent through the second half of 2021 that output was only 1.1% down on the same point in 20192. This is remarkable, given the sharp falls in the first half of the year, and indicates that we should return to pre-COVID levels sometime in the first half of this year (although return to trend will take longer).

Continued strong economic growth has immediate implications for incomes and house prices, and risks providing a solid platform for continued exuberance in housing.

Lending standards

In the past, house prices have been significantly affected as a result of changes made by APRA to regulations around lending standards for residential property3. The relaxation of these regulations in the period prior to the pandemic is arguably contributing to the availability of capital in the current boom, and since an interest rate rise is out of the question for the moment, it’s likely that the regulators will reach yet again for macro-prudential controls to slow housing lending and contain risk in the sector.

These actions don’t target house prices per se, but past experience indicates that surging house prices leads to a deterioration in lending standards and increasing risks to financial stability. And the metrics in front of the regulators at the moment show record housing finance, pointing to an acceleration in housing debt, an increasing share of lending at high loan to valuation (LVR) ratios and a rising share of interest-only loans, albeit from a low base.

All of this suggests that APRA could start tapping the lending standards brake soon, firstly by increasing interest rate buffers but potentially also by reintroducing limits on high LVR lending and restricting loans to customers with lower serviceability.

The effects of changing living patterns

Deferred spending has played a major role in driving housing demand through the pandemic; most salary-earners who kept their jobs were relatively unaffected by the downturn but had fewer opportunities to spend and so some focussed more on their home. This effect is likely to lessen as borders begin to re-open and travel resumes to a larger degree, but there are other lifestyle patterns that stand to endure beyond the end of the pandemic.

Lower rates of immigration (which disproportionately affects urban demand) and the secular trend towards working from home are two such factors, and both have contributed towards the outperformance of regional dwelling prices mentioned earlier (although regional property was also less exposed to indebtedness).

They are also helping to drive a growing disconnect between house and unit prices. Capital city house prices rose 3.1% in March and 6% over the last 12 months, whereas unit prices lagged with a 1.9% gain in the month and 1.1% rise on a year ago. This also reflected a disparity in rental movements between the two property classes, with average unit rents falling 3.8% compared to a 5.2% rise in house rents.

The immigration deficit will be resolved over time, although it is becoming clear that international borders will open more slowly than many were expecting. The trend to decentralised working will be more resilient, and governments may even consider encourage working from home as a way to take pressure off capital city prices over the longer term.

There have been other important influences at work in the housing market over the past year, including internal dynamics, such as the fear of missing out and the initial reluctance of property owners to sell into a falling market (which supported prices through the worst of the pandemic). Prices could also soon approach levels where poor affordability starts to significantly affect demand.

In the meantime, we can expect prices to rise another 15-20% over the next 18 months to two years, with the pace of growth slowing though 2021-22 as inflation starts to pick up and interest rate rises move back onto the agenda.

1 APRA (2021), Temporary loan repayment deferrals due to COVID-19, February 2021

2 https://www.ampcapital.com/au/en/insights-hub/articles/2021/march/december-quarter-gdp-numbers-show-a-strong-rebound-but-further-recovery-will-be-slower

3 Bullock M. & Orsmond D. (2019), House Prices and Financial Stability: An Australian Perspective, In Nijskens R., Lohuis M., Hilbers P. & Heeringa W. (eds) Hot Property: The Housing Market in Major Cities pp 195-205, Springer, Cham.

Reproduced with the permission of the AMP Capital. This article was originally published at https://www.ampcapital.com/au/en/insights-hub/articles/2021/april/four-factors-besides-interest-rates-that-will-shape-the-outlook-for-house-prices

While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) (AMP Capital) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent of AMP Capital.

This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.