Dr Shane Oliver – Head of Investment Strategy and Chief Economist, AMP Capital

Key points

-

Inflation is placing increasing pressure on major central banks to remove monetary stimulus.

-

Inflation & rising interest rates will likely contribute to more volatile & constrained investment returns this year.

-

The long-term downtrend in inflation and interest rates since the early 1980s is likely to be over removing a tailwind for investment returns.

Introduction

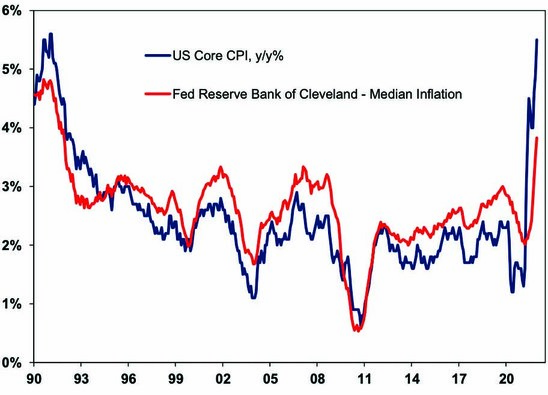

For last few decades inflation has not been much of an issue. It was all about economic activity. Books were even written about “the death of inflation”. In fact, for much of the post GFC period inflation in many countries was below central bank targets and all the talk was of “secular stagnation” and disinflation with a fear of deflation. Since around May last year though following a surge in inflation in many emerging countries and notably the US it’s become more of an issue. In fact, US inflation rose to 7% in December, a near 40 year high. Even inflation excluding food and energy in the US has risen to 5.5%, a 30 year high.

US Inflation Measures

Source: Bloomberg, AMP

This is pressuring central banks to remove monetary stimulus. But what’s driving higher inflation? Is it likely to settle down this year? What’s the longer-term inflation outlook? What will it mean for interest rates? What will it mean for investment markets? And what are the best hedges against inflation?

Why does inflation matter for investors?

But before we look at these issues its worth considering why it’s important for investors. Until only a year ago all the talk was about the need to get inflation back up. So what’s all the fuss?

Inflation refers to a generalised and persistent rise in the price of goods and services. When it’s too low – say around 1% or less – it runs the risk of slipping into deflation which has often been associated with depression and makes it harder for central banks to achieve interest rates low enough to stimulate economic growth. But when inflation is too high it tends to be associated with lower productivity, as much economic activity is directed towards protecting against inflation, shorter economic cycles and more uncertainty – as was seen in the high inflation 1970s. So central banks in developed countries have aimed for the happy medium of around 2% inflation per annum.

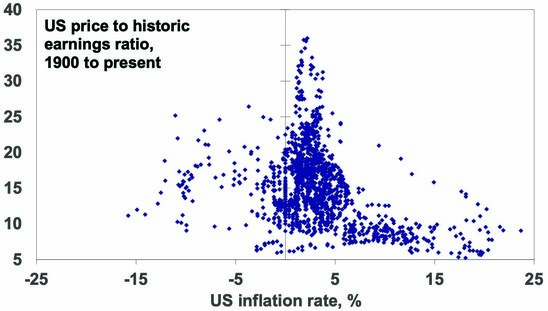

For investment markets high inflation tends to be bad as it means: higher interest rates; higher economic volatility and uncertainty; and for shares, a reduced quality of earnings as firms tend to understate depreciation when inflation is high. All of which means that shares tend to trade on lower price to earnings multiples when inflation is high, and growth assets generally tend to trade on higher income yields. This was seen in the high inflation 1970s when shares struggled. Of course, shares also don’t like recession and depression associated with deflation so the best inflation level for the share market is around 2% inflation as it tends to be associated with the highest PE on US shares.

US shares – Higher inflation = lower PEs

Source: Bloomberg, AMP

So the bottom line is that a sustained period of high inflation can be a problem for shares and other growth assets.

What’s driving the rise in inflation?

The key drivers of the rebound in inflation are a combination of:

-

base effects – as 2020’s deflation dropped out of annual calculations, although we have now gone well beyond that;

-

a surge in demand for goods versus services due to lockdowns, stimulus payments & pent up demand;

-

supply struggling to keep up, not helped by worker shortages (resulting in faster wages growth), geopolitical tensions impacting energy prices and higher transportation costs given the supply bottlenecks.

-

higher commodity prices as investment surged; and

-

reopening leading to a rebound in some prices.

Initially, it was narrowly based on a few categories subject to reopening, but it has broadened out with the median level of US CPI components’ inflation rates rising sharply and 75% of US CPI components seeing inflation above 3%yoy. In a big picture sense, the surge in inflation in the US is consistent with a large increase in its money supply, which has fed through to demand via significant fiscal easing. The further supply side disruptions associated with the Omicron wave are not helping.

While inflation is generally weaker in other developed countries – partly due to less monetary and fiscal stimulus – it has increased. In Europe and the UK its around 5%yoy. In Australia its around 3%yoy, although that’s down from 3.8%yoy. By contrast in China its just 1.5%yoy and in Japan its 0.6%yoy.

Will inflation settle down this year?

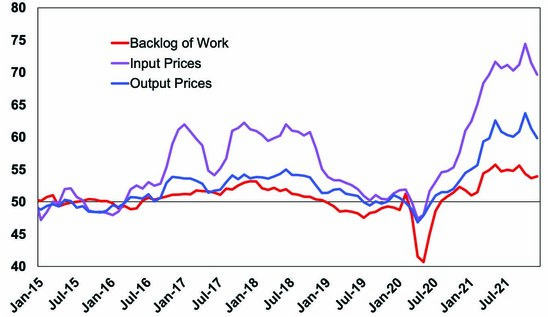

The spike in inflation has gone on for longer than first expected forcing the Fed to ditch use of the word “transitory” when describing it. This has been partly due to ongoing disruption from coronavirus waves which have kept goods demand up and constrained supply. However, some fall back in inflationary pressures is likely this year as goods demand retreats from levels well above trend, in favour of services, and as production improves. There are some tentative signs of this, with input and output prices rolling over in global business conditions (PMI) surveys, the Baltic Dry shipping cost index down from its highs and producer price indexes showing some loss of momentum.

Flash Manufacturing PMI Indices, Global Average

Source: Bloomberg, AMP

But is higher inflation likely to become the new norm?

The pandemic has likely changed many things, which combined with various other forces are likely to mean an end to the period of post GFC “secular stagnation”. A bit like World War Two finally put an end to the deflationary forces of the 1930s. In a longer-term context, we are likely seeing the bottoming of the long-term decline in inflation since the early 1980s:

-

2020 saw central banks start to take a far more aggressive approach to pushing up inflation. Massive money printing was combined with massive fiscal stimulus (particularly in the US) which provided a means for easy money to boost spending (unlike last decade when fiscal austerity offset easy money). A shift from focussing on forecast to actual inflation also meant central banks will be slower to raise rates allowing inflation to rise further which is what we saw last year in the US. This constituted a “regime shift” in the approach to boosting inflation – much like the aggressive approach to keeping inflation down led by the Fed from the early 1980s was a “regime shift”.

-

We’re seeing a trend to bigger governments and that can ultimately be associated with lower productivity growth.

- Globalisation appears in decline, as a result of geopolitical tensions and onshoring, meaning less competition.

-

The ratio of workers to consumers is declining in many countries which may drive higher wages growth and lower productivity growth. The pandemic appears to have accelerated this problem by boosting retirement in some countries like the US (although its less evident in Australia) and it refocused workers on quality-of-life considerations making them more demanding in terms of pay.

The bottom line is that many of the factors that drove the declining trend in inflation since the early 1980s are now fading. In this context the current spike in inflation is likely part of a longer-term bottoming process. However, it’s not all one way (technological innovation is still bearing down on prices, and the pandemic may work to drive more productivity) and the 1960s showed us the bottoming of inflation may take years to play out. But it all likely suggests that the long-term decline in inflation since the early 1980s and the downtrend in interest rates and bond yields that it largely drove are over. This will likely remove a tailwind from share and other growth asset returns.

How will central banks react?

Central banks started to remove monetary stimulus last year. Several have already raised rates – in the UK, Norway, Korea & NZ. After seeing the spike in inflation for much of last year as “transitory” the Fed has now ditched the term and is moving to remove monetary stimulus faster. It may end its quantitative easing bond buying program this month and we expect it to start raising rates in March, with four or five rate hikes this year and start quantitative tightening in the second half.

The RBA is lagging behind the Fed and for good reason as inflationary pressures are less in Australia. Inflation here is less than half what it is in the US, only about a third of CPI items are seeing inflation above 3%yoy compared to 75% in the US and wages growth is only 2% here compared to around 4.5% in the US. However, despite another temporary coronavirus setback with Omicron, growth is likely to be strong this year pushing unemployment down to 4% and the pace of wages growth up to 3% later this year and so we see the RBA starting to raise the cash rate in November and taking it to 0.5% by year end. And it’s likely to end quantitative easing in either February or May.

By contrast, the ECB is unlikely to start raising rates till next year. Rate hikes in Japan with zero inflation are likely years away. And China’s central bank has started to ease monetary policy and will likely ease further to boost growth.

Implications for investment markets

The higher levels of inflation and more major central banks removing monetary stimulus will result in a constrained and volatile ride for investment markets this year:

-

Bond yields are likely to drift higher as it becomes clear that inflation will remain higher for longer. This likely means another year of capital losses on bonds.

-

First rate hikes in tightening cycles cause volatility in shares but Fed and RBA rate hikes this year are unlikely to be enough to bring an end to the cyclical bull market as monetary policy is unlikely to be pushed into tight territory.

-

Rising fixed mortgage rates and then from later this year rising variable rates are expected to slow home price gains to 5% this year and push prices down next year as higher rates restrict the amount new buyers can borrow.

Of course, if inflation gets out of control and looks like staying well above central bank inflation targets the valuation boost from low inflation and low interest rates will start to be reversed, resulting in poor returns from growth assets. This is not our base case, but it’s a risk.

What are good hedges against higher inflation?

For those worried about a return to much higher inflation driving much higher bond yields and weighing on sectors like high PE tech stocks, the best protection remains inflation-linked bonds, real assets (like commodities) and parts of the share market that will see stronger earnings growth.

Source: AMP January 2022

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.