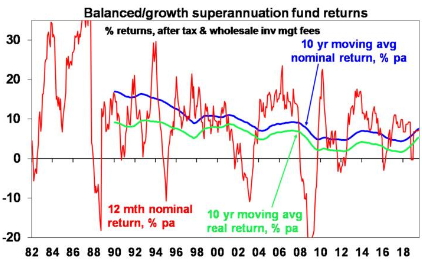

The past 10 years have seen pretty good returns for well-diversified investors. The median balanced growth superannuation fund returned 7.3% pa over the five years to July and 8.2% pa over 10 years and that’s after fees and taxes. This is impressive given that inflation has been around 2%.

Source: Mercer Investment Consulting, Morningstar, AMP Capital

Shares and growth assets have literally climbed a wall of worry this decade with a revolving door list of worries around public debt, the Eurozone, deflation, inflation, rate hikes, Trump, North Korea, China, trade wars, growth, house prices, etc. But returns benefitted from the recovery after the GFC and a search for yield as interest rates have collapsed depressing yields on most assets. But – while it sounds like a broken record – the decline in yields points to eventually more constrained returns ahead.

Declining yields = falling medium-term return potential

Investment returns have two components: yield (or income flow) and capital growth. Looking at both of these components points to lower average investment returns over the next five years compared to the last five years. It’s basic to investing that the price of an asset moves inversely to its yield all other things being equal. Suppose an asset pays $10 a year in income and suppose its price is $100, which means an income flow or yield of 10%. If interest rates are cut resulting in increased demand for the asset, as investors search for a higher yield, such that its price rises to $120 given the $10 annual income flow its yield will have fallen to 8.3% (ie $10 divided by $120) as its price has gone up by 20%. So, yield moves inversely to price. But as yields decline it means a lower return potential going forward.

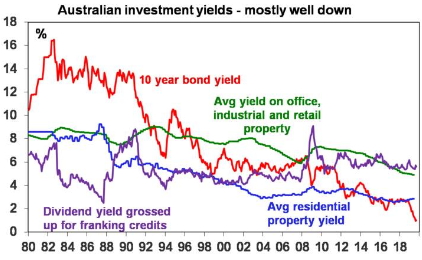

Since the early 1980s investment yields have collapsed. Back then the RBA’s “cash rate” was around 14%, 1-year bank term deposit rates were nearly 14%, 10-year bond yields were around 13.5%, commercial and residential property yields were around 8-9% and dividend yields on shares were around 6.5% in Australia and 5% globally. This meant that investments were already providing very high income so only modest capital growth was needed for growth assets to generate good returns. So, most assets had very strong returns and balanced growth super fund returns averaged 14.1% in nominal terms and 9.4% in real terms between 1982 and 1999 (after taxes and fees).

Over the last four decades, investment yields have mostly fallen quite sharply. See the next chart.

Source: Bloomberg, REIA, JLL, AMP Capital

Today the cash rate is 1%, 1-year bank term deposit rates are 1.5%, 10-year bond yields are 0.9%, gross residential property yields are around 3%, commercial property yields are just below 5%, dividend yields are still around 5.5% for Australian shares (with franking credits) but they are 2.5% for global shares. This points to a lower return potential for a diversified mix of assets.

What’s more, the capital growth potential from growth assets is likely to be constrained relative to the past reflecting more constrained nominal economic growth. Several megatrends are likely to impact growth over the medium term. These include:

-

Continued slower growth in household debt.

-

An ongoing retreat from globalisation, deregulation and small government in favour of populist, less market friendly policies.

-

A shift in corporate focus from profit to “balanced scorecards”.

-

Rising geopolitical tensions – notably as the US attempts to constrain the rising power of China as evident in the trade war.

-

Aging and slowing populations – resulting in slowing labour force growth and rising pressure on public sector budgets.

-

Technological innovation and automation.

-

Continuing rapid growth in Asia and China’s middle class.

-

Pressure to slow emissions & the impact of global warning.

-

A large shift to sustainable energy as its cost continues to fall.

Most of these will constrain economic growth & hence returns.

Medium-term return projections

Our approach to get a handle on medium-term return potential is to start with current yields for each asset class and apply simple and consistent assumptions regarding capital growth reflecting the above-mentioned megatrends. We also prefer to avoid forecasting and like to keep the analysis simple.

-

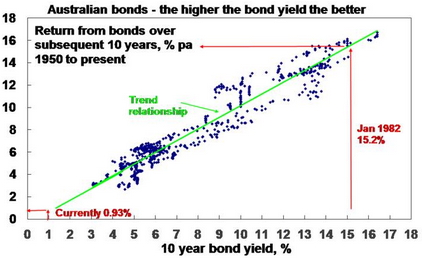

For bonds, the best predictor of future medium-term returns is current bond yields as can be seen historically in the next chart. If a 10-year bond yield is held to maturity its initial yield (0.93% right now in Australia) will be its return over 10 years (ie 0.93%). We use 5-year bond yields as they more closely match the maturity of bond indexes.

Source: Global Financial Data, Bloomberg, AMP Capital

-

For equities, current dividend yields plus trend nominal GDP growth (a proxy for capital growth) does a good job of predicting medium-term returns.1

-

For property, we use current rental yields and likely trend inflation as a proxy for rental and capital growth.

-

For unlisted infrastructure, we use current average yields and capital growth just ahead of inflation.

-

In the case of cash, the current rate is of no value in assessing its medium-term return. So we allow for some rise in cash rates over time.

Our latest return projections are shown in the next table.

Projected medium term returns, %pa, pre-fees and taxes

|

Current |

+ Growth |

= Return |

|

|

World equities |

2.6^ |

4.1 |

6.6 |

|

Asia ex Japan equities |

1.6^ |

6.9 |

8.5 |

|

Emerging equities |

1.9^ |

6.9 |

8.9 |

|

Australian equities |

4.3 (5.7*) |

3.2 |

7.5 (8.9*) |

|

Unlisted commercial property |

4.9 |

1.7 |

6.6 |

|

Australian REITS |

4.6 |

2.3 |

6.7 |

|

Global REITS |

3.6^ |

1.6 |

5.5 |

|

Unlisted infrastructure |

4.6^^ |

3.0 |

7.6 |

|

Australian bonds (fixed interest) |

1.1 |

0.0 |

1.1 |

|

Global fixed interest ^ |

1.3 |

0.0 |

1.3 |

|

Australian cash |

2.0 |

0.0 |

2.0 |

|

Diversified Growth mix * |

|

|

5.6 |

# Current dividend yield for shares, distribution/net rental yields for property and duration matched bond yield for bonds. ^ Includes forward points. * With franking credits added in. Source: AMP Capital.

The second column shows each asset’s current income yield, the third shows their 5-10 year growth potential, and the final column their total return potential. Note that:

-

We assume inflation averages around or just below central bank targets.

-

For Australia we have adopted a relatively conservative growth assumption reflecting slower productivity growth.

-

We allow for forward points in the return projections for global assets based around current market pricing.

Key observations

Several things are worth noting from these projections.

-

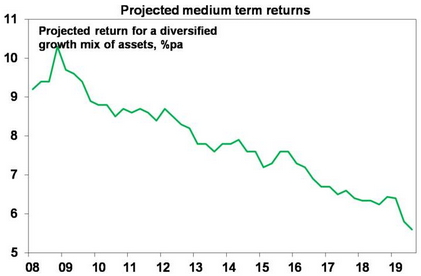

The medium-term return potential has continued to fall due largely to the rally in most assets and fall in investment yields. Projected returns using this approach for a diversified growth mix of assets have fallen from 10.3% pa at the low point of the GFC in March 2009, to 8.6% five years ago, to 6.2% a year ago and to now just 5.6%.

Source: AMP Capital

-

Government bonds offer low returns due to ultra-low yields. Yes, bond returns have been strong lately as yields have collapsed pushing up bond prices. But this is no guide to future returns, particularly if bond yields stop falling.

-

Unlisted commercial property and infrastructure continue to come out relatively well, reflecting their higher yields.

-

Australian shares stack up well on the basis of yield, but it’s still hard to beat Asian/emerging shares for growth potential.

-

The downside risks to our medium-term return projections are that: the world plunges into a recession driving another major bear market in shares or that investment yields are pushed up to more normal levels as inflation rebounds causing large capital losses. Just allow that drawdowns in returns tend to be infrequent but concentrated and it’s been a while since the last big one. See the first chart.

-

The upside risks are (always) less obvious but could occur if we see improving global growth but inflation remaining low.

Implications for investors

-

First, have reasonable return expectations. Low yields & constrained GDP growth indicate it’s not reasonable to expect sustained double-digit or even high single digit returns. In fact, the trend decline in the rolling 10-year average of both nominal and real super fund returns since the 1990s indicates we have been in a lower-return world for many years – it’s just that it only becomes clear every so often with bear markets and then strong returns in between.

-

Second, remember that responding to a lower return potential from major asset classes by allocating more to growth assets does mean taking on more risk.

-

Third, bear markets are painful, but they do push up the medium-term return potential of investment markets to higher levels and so provide opportunities for investors.

-

Fourth, some of the decline in return potential reflects very low inflation – real returns haven’t fallen as much.

-

Finally, focus on assets with decent sustainable income flow as they provide confidence regarding future returns.

Source: AMP Capital 25 September 2019

1Adjustments can be made for: dividend payout ratios (but history shows retained earnings often don’t lead to higher returns so the dividend yield is the best guide); the potential for PEs to move to some equilibrium level (but forecasting the equilibrium PE can be difficult and dividend yields send valuation signals anyway); and adjusting the capital growth assumption for some assessment regarding profit margins (but this is hard to get right). So, we avoid forecasting these things.

Important notes: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) (AMP Capital) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent of AMP Capital.