– shares are vulnerable to a bout of volatility but here’s five reasons why the trend will likely remain up

Introduction

From their lows last October, it has been relatively smooth sailing for shares – with US shares up 28%, global shares up 25% & Australian shares up 17% to recent highs. But the last few weeks have seen a rough patch with renewed concerns about interest rates and fears of an escalation in the war around Israel to include Iran (after Iran fired missiles & launched drones at Israel in retaliation for an attack on its consulate in Syria). The obvious issue is how vulnerable are shares? Could the bull market that got under way from the inflation and interest rate lows of 2022 (that has seen global shares rise 42% and Australian shares rise 23%) be over?

The worry list for shares

The bull market since the 2022 lows has been driven by optimism that inflation is falling enabling central banks to lower interest rates at the same time that economic growth has held up better than feared resulting in a sort of Goldilocks – not too hot and not too cold – scenario. But after such strong gains there is now a significant worry list for shares.

-

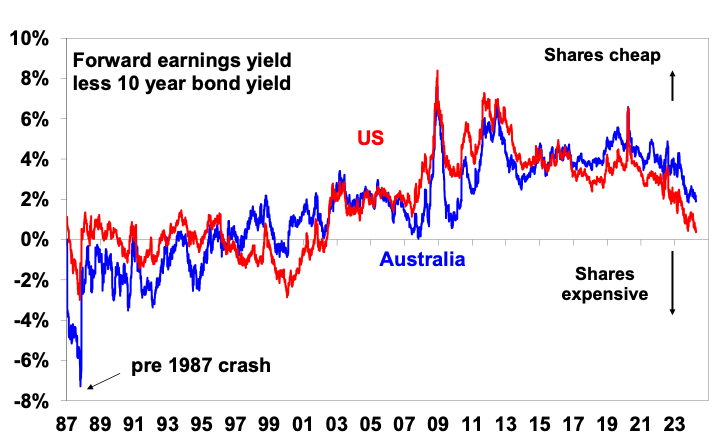

First, share market valuations are stretched. The next chart shows that the risk premium offered by shares over bonds – proxied by the gap between forward earnings yields and 10-year bond yields – has fallen to its lowest since the early 2000s in the US. Australia is a bit more attractive, but the premium is still near the lowest since 2010.

Equity risk premium over bonds

Source: Bloomberg, AMP

-

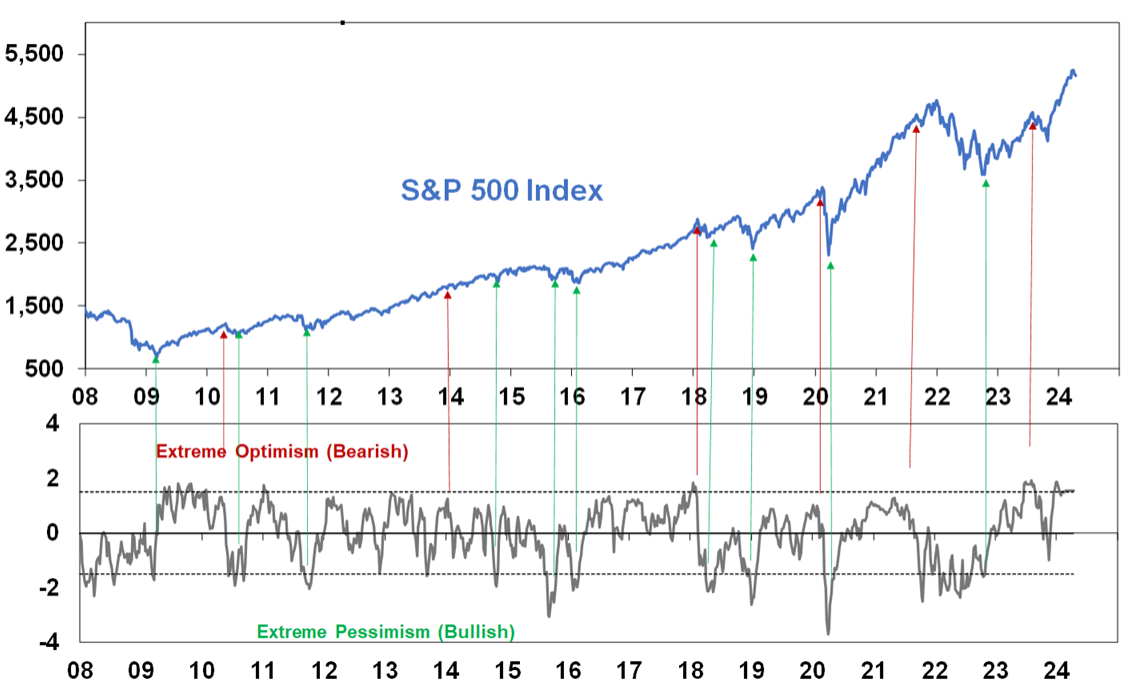

Second, US investor sentiment is at levels that can warn of corrections (red arrows). It’s not a super reliable timing indicator but it is back to levels seen last July prior to the 10% fall in shares into October.

Composite Investor Sentiment vs US shares

Sentiment index based on a composite of surveys of investors and investment advisers and options positioning. Source: Bloomberg, AMP

-

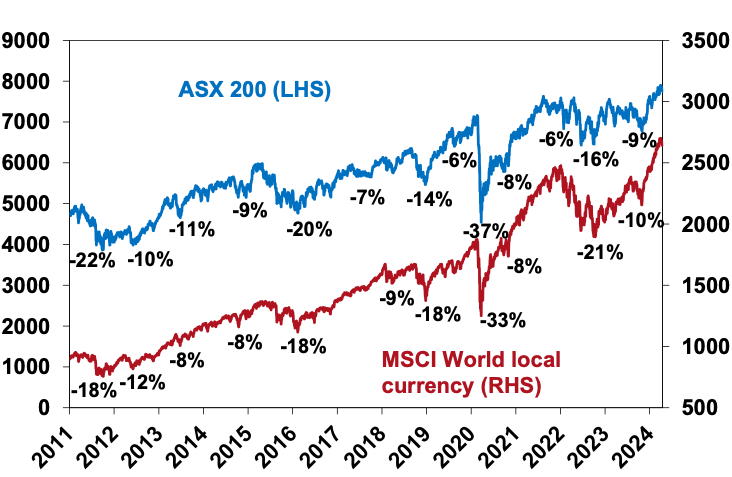

Thirdly, after strong gains shares have become technically overbought, but it’s normal to have 5% plus pullbacks every so often.

Periodic share market pull backs are normal

Source: Bloomberg, AMP

-

Fourth, uncertainty over when the Fed will start to cut rates has been increased by three worse than expected monthly CPI inflation results in a row as a result of sticky services inflation. This has seen money market expectations for 0.25% rate cuts this year scaled back from 7 starting in March this year to now less than two starting in September. And in Australia they have been scaled back from nearly three starting in June to no rate cut until late this year/early next.

-

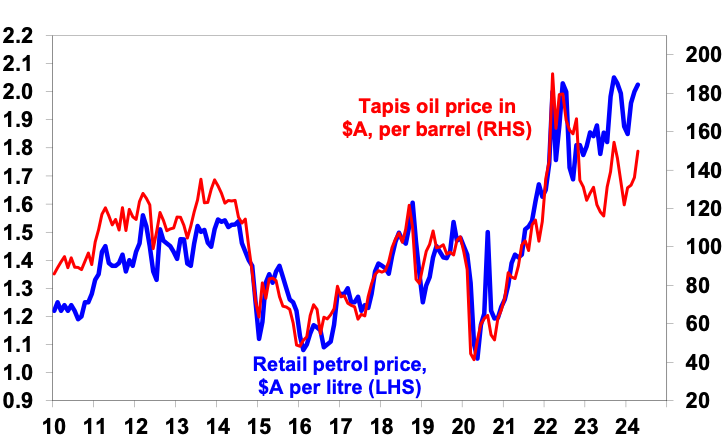

Fifth, Iran’s retaliatory attack on Israel risks an escalation depending on how Israel responds. This would threaten Iran’s 3% of world oil production and the flow of oil through the Strait of Hormuz (through which roughly 20 million barrels a day or 20% of world oil production flows mainly enroute to Asia). Another sharp spike in oil prices would be a threat to the economic outlook as it could boost inflation again and risk adding to inflation expectations potentially resulting in higher than otherwise interest rates and act as a tax hike on consumers leaving less to spend on other things. Australian petrol prices are already around record levels despite oil prices still being well below their 2022 highs because of the rise in oil prices this year and wider refinery margins. A spike in world oil prices from around $US85/barrel for West Texas to around $US100/barrel would add around $15cents/litre to average Australian petrol prices and push the weekly household petrol bill in Australia to a record $76 up $10 a week from where it was a year ago. This would mean more than $500 less a year for the average family available to spend on other things.

Australian petrol prices versus Tapis oil price

Source: Bloomberg, AMP

-

Sixth, the US presidential election threatens to cause volatility particularly if it looks like former President Trump will be returned. His policies to lower taxes would be taken positively by the US share market as they were in 2017, but his talk of raising tariffs (10% on all imports and 60% or more on Chinese imports) threatening higher inflation and an all out trade war would be negative. In his first term he went with tax cuts first (shares surged in 2017) then tariffs (shares slumped in 2018), but he may go with tariffs first if he wins this time.

-

Finally, while the global economy has held up well, the risk of recession remains high as the full impact of the monetary tightening since 2022 continues to feed through as things like savings buffers built up through the pandemic are run down. Chinese growth also remains at risk given the ongoing weakness in its property sector.

In short, the combination of stretched valuations, high levels of investor optimism and technically overbought conditions leave shares potentially vulnerable to a further pull back. Geopolitical risks including events in the Middle East, delays to rate cuts and recession risks could provide a trigger.

Five reasons for optimism

However, while shares may be vulnerable a pull back and a period of increased volatility, several considerations suggest that the bull market will remain intact and the trend in shares will remain up.

First, US, global shares and Australian shares are still tracing out a pattern of rising lows and highs from 2022, which is still consistent with a bull market. Similarly, we have yet to see the sort of churning and a declining trend in the proportion of stocks making new highs that normally comes at major share market tops. And while many worry about a new tech bubble (and have done for years) the tech and AI centric stocks of today make real profits so Nasdaq’s PE is around 35 times, not the 100 times plus it was at the tech bubble high in 2000.

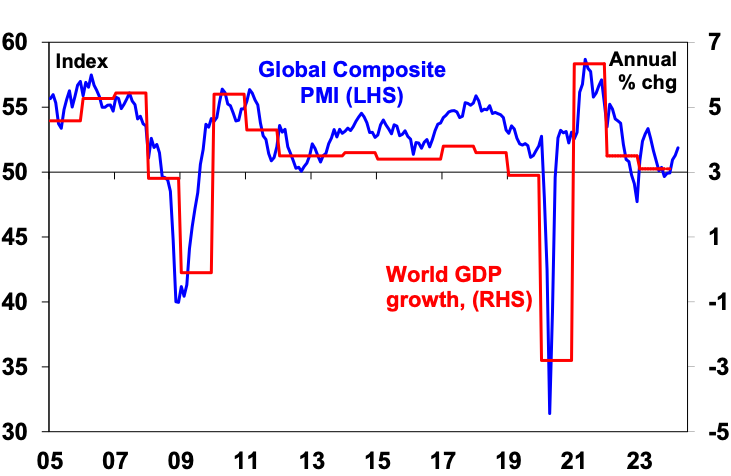

Second, while there are areas of weakness, global and Australian economic conditions generally continue to hold up far better than feared. In fact, business conditions according to purchasing manager surveys (PMIs) have improved recently. Consistent with this, profits have generally held up better than expected – while down slightly in Australia they have increased more than expected in the US and March quarter earnings results are likely to show a continuation of this.

Global Composite PMI vs World GDP

Source: Bloomberg, AMP

Third, despite the relative resilience of economic activity inflation has fallen sharply globally (from highs around 8% to 11% to around 3%) and will likely keep falling allowing rate cuts. Although the US has proven a bit stickier in the last three months reflecting its stronger economy, inflation has continued to fall in other countries. And even in the US, cooling measures of labour market tightness are continuing to point to lower services inflation ahead. It’s a similar picture in Australia. So, while rate cuts have been delayed, they are still likely.

Fourth, while Chinese economic growth is not as strong as it used to be it seems to be hanging in there around 5% despite its property slump. While the iron ore price has recently fallen it remains in the same range it’s been in for the last two and a half years and well above many assumptions. Furthermore, the copper price appears to be breaking higher which is normally a sign of strength.

Finally, while geopolitical risks are high, they may not turn out the be as bad as feared – much as was the case last year:

-

While the risk of an escalation between Israel and Iran is high – Iran’s retaliation to the attack on its Syrian consulate was similar to its response when General Soleimani was killed by the US in in 2020. It was well flagged, measured and there was minimal damage and designed not to provoke a bigger Israeli counter-retaliation. The US is also pressuring Israel to hold back and of course is motivated by trying to keep oil prices down in an election year. So far so good so markets have not gone into free fall and the oil price has not surged. Hopefully that remains the case, but there is a way to go yet.

-

There is still a long way to go in the US election.

-

It’s worth bearing in mind the response of shares to past geopolitical events. An analysis by Ned Davis Research on a range of crisis events back to WW2 shows an initial average 6% fall in US shares, but with shares up an average 6%, 9% and 15% over the subsequent 3, 6 and 12 months. Of course, there is a huge range around that!

Implications for investors

We remain of the view that shares will do okay this year as central banks ease. But given the long worry list, global and Australian shares are vulnerable to a correction or at least a more volatile and constrained ride than seen so far this year. For most investors though the key is to recognise that share market pullbacks are healthy and normal, it is very hard to time market moves and the best way to grow wealth is to adopt an appropriate long term investment strategy and stick to it.

Dr Shane Oliver – Head of Investment Strategy and Chief Economist, AMP

Source: AMP Capital April 2024

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.